Globally we are facing enormous energy challenges. The social shocks that rocked the world during the Covid-19 pandemic and associated lockdowns, followed by geopolitical turmoil has precipitated an energy crisis in Europe.

The energy crisis – or energy trilemma – covers three principal areas:

- The cost of energy;

- Energy security; and

- Net zero.

1) The cost of energy

Energy costs are stressing the world’s economy, particularly Europe’s, in a way that hasn’t been seen for decades.

Energy prices started to rise as we came out of the pandemic. When Russia invaded Ukraine in February 2022 this added further pressure and triggered a large inflationary spiral – and the impact on energy prices has been stark.

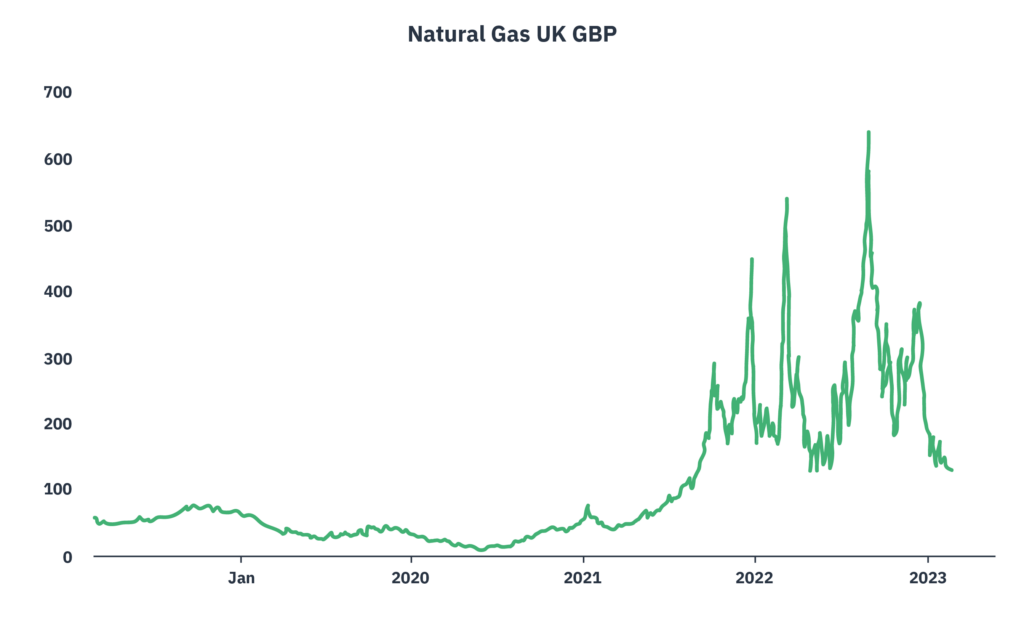

Looking at the UK’s gas market, winter prices for 2022 hit historic highsi.

European gas prices reached record highs in August 2022

2) Energy Security

The second part of the trilemma is energy security.

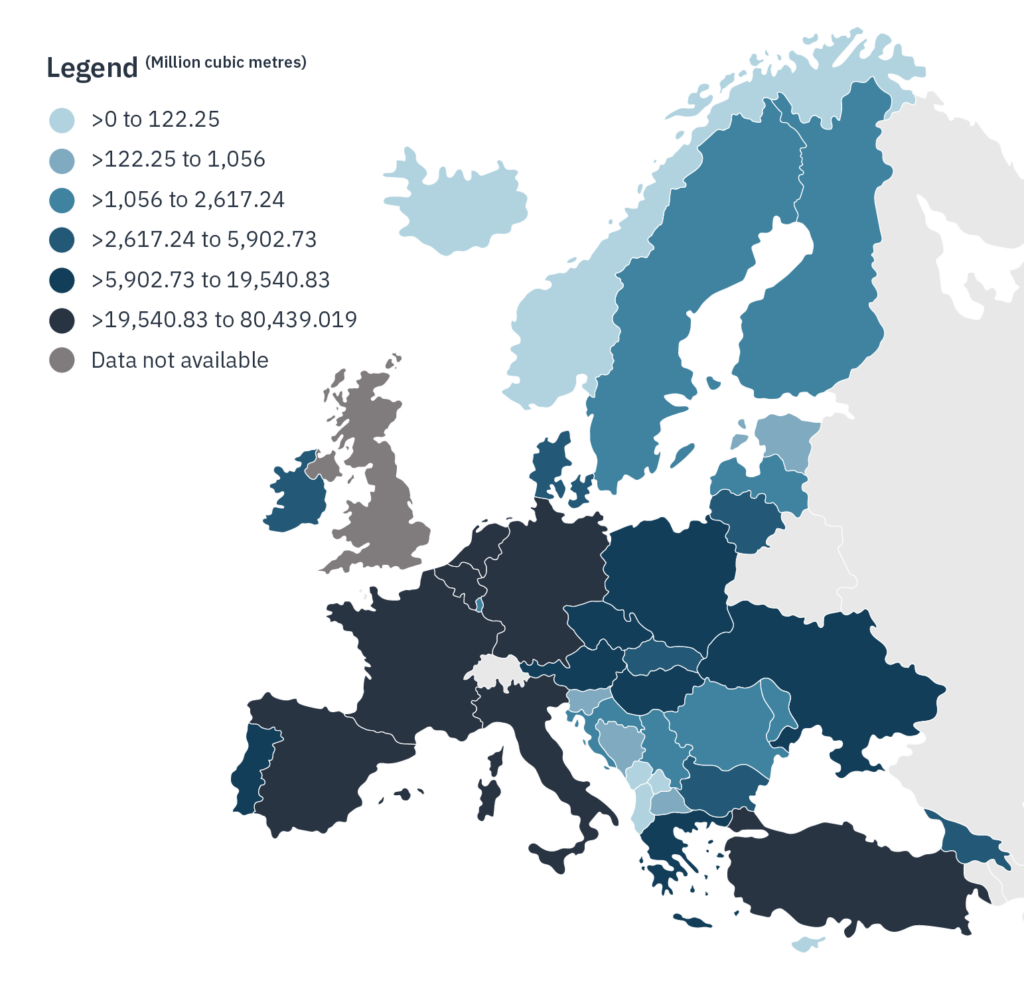

In 2020, the EU was dependent on imports for 57.5% of its energyii with a particularly heavy reliance on Russian gas. Germany and Italy were particularly exposed with 65% and43% of their gas supplies respectively dependent upon Russianiii.

Imports of Russian gas by country,2020

3) Net Zero

The final part of this trilemma is the progression to Net Zero.

What does Net Zero mean? Internationally scientists agree that in order to prevent the worst impacts of climate change we need to limit global warming to 2 degrees centigrade above average temperatures before global industrialisation took off in the mid-19th century. To achieve this change, global net human-caused emissions of carbon dioxide (CO2) need to fall by about 45% from 2010 levels by 2030, to reach Net Zero by 2050iv.

The horror of the Russian invasion of Ukraine and the general geopolitical tensions that have been on show throughout 2022 have meant that global Net Zero ambitions to combat climate change have been less of a focus for global leaders and policy makers. Yet many would argue that climate change and the transition required to address it are the greatest global challenges of our generation.

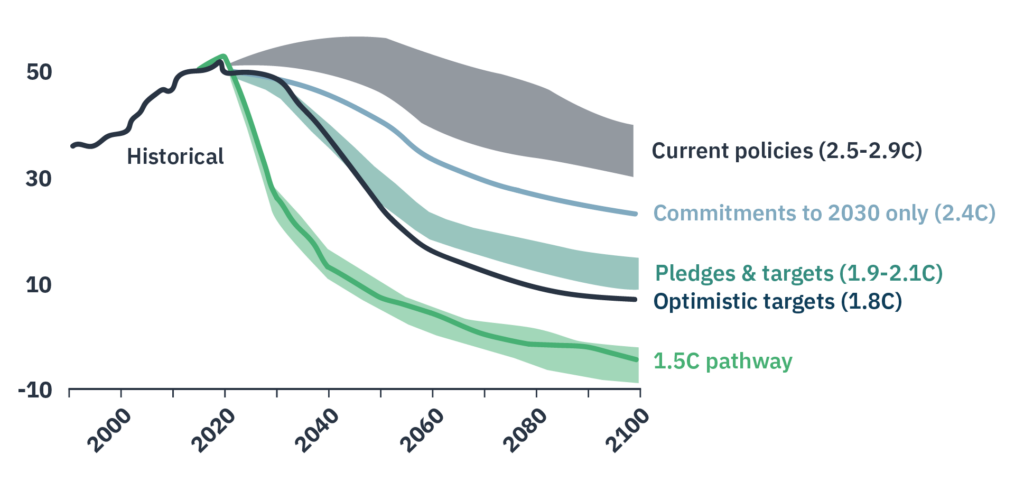

The good news is that we’ve started to address the situation. The bad news is that we are a long way away from where we need to be. According to the United Nations we need to be reducing emissions by 45% by 2030, but we are instead on track to increase these by + 10%v.

Global greenhouse gas emissions in gigatons of carbon dioxide equivalent

The role renewable energy and storage can play in alleviating the energy crisis

Renewable energy has a big role to play in dealing with climbing energy costs, energy instability, and achieving Net Zero targets, by offering cheaper more reliable (both physically and geo-politically) and more sustainable sources of energy .

Energy costs

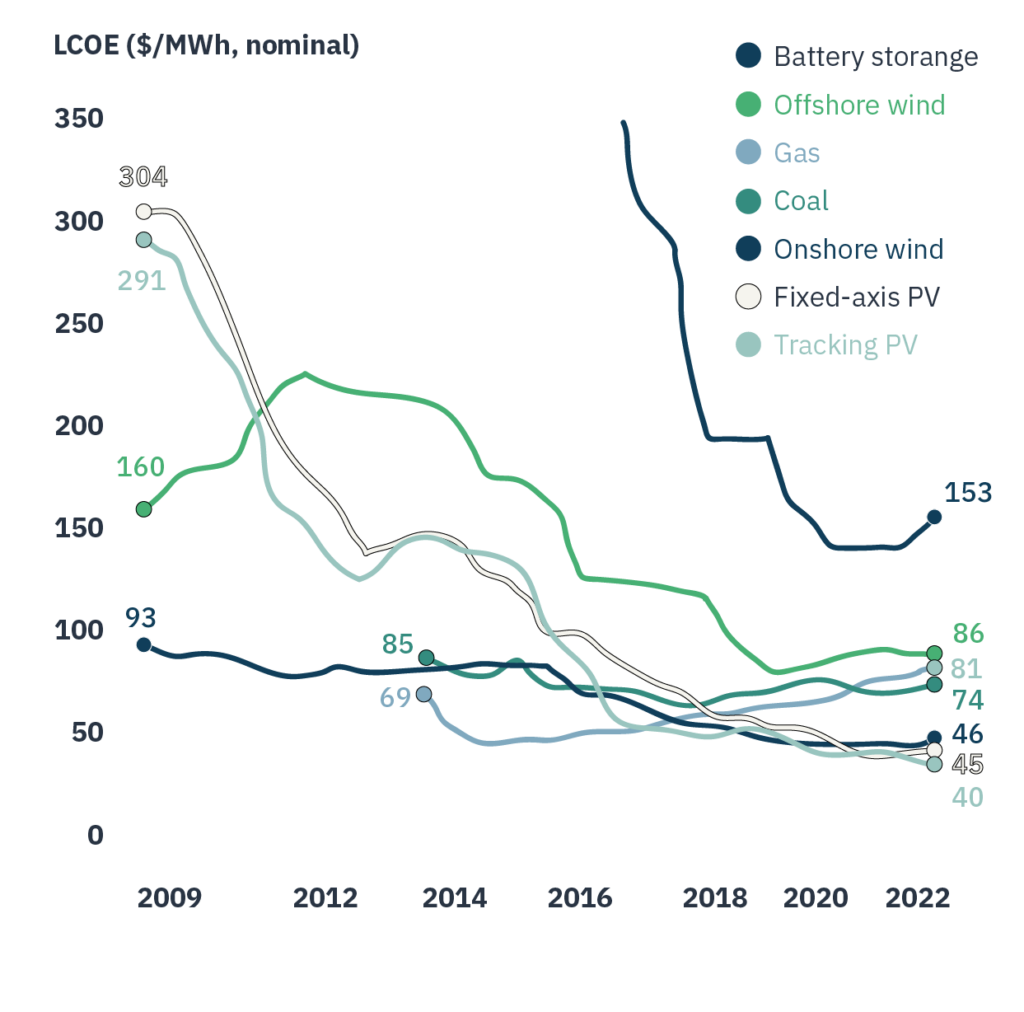

Most of us are living in a region where solar or wind are the cheapest forms of energyvi. This is partly due to the significant reduction in the cost of solar and wind energy over the past decade – with solar reducing by over 90% to less than the costs of traditional energy sources such as coal and gasvii. It is remarkable how fast this has happened. In 2015, solar or onshore wind were the cheapest forms of energy for only 1% of the world’s population. By 2021 this had risen to 66% and covered 71% of global GDPviii. This is extraordinarily influential in the story of global energy markets, and on its own is a strong argument for a renewable-driven energy future.

Global levelized cost of electricity benchmarks

An important driver of this cost reduction is the removal of Government subsidies needed to support the renewable energy sector. This shift has opened renewables to investment in markets where the geo-political risk of subsidies would have, historically, made investing unattractive.

The other important technology to consider is battery storage. The challenge with renewable energy is that it is intermittent, meaning energy systems become vulnerable when the sun doesn’t shine, or the wind doesn’t blow. Battery technology is now a highly cost-effective way of balancing the system by creating a proxy for a baseload. Whilst we may always need gas as a proportion of energy supply, we are moving to a place where we do not need, or want, to be dependent on it.

Energy Security

The Russian war in Ukraine and Putin’s weaponisation of energy markets has highlighted the dangers to European governments of having such a heavy reliance on a single provider of energy.

Governments and investors have historically proven to have short memories, but it seems likely that this may be one of those events that causes a radical and lasting change in behaviour.

If Europe wishes to wean itself off Russian gas quickly it has two options:

- Go to other gas producers around the world to source energy – something that is happening but is both more expensive and it is negatively impacting poorer nations who can no longer source their energy.

- The increasing opportunity of technologies that can balance the grid, such as batteries which enable solar and wind to be far more effective. The advantage of renewable energy – specifically solar and wind – is that it can be deployed very quickly creating a diversified, distributed grid.

Net Zero impact

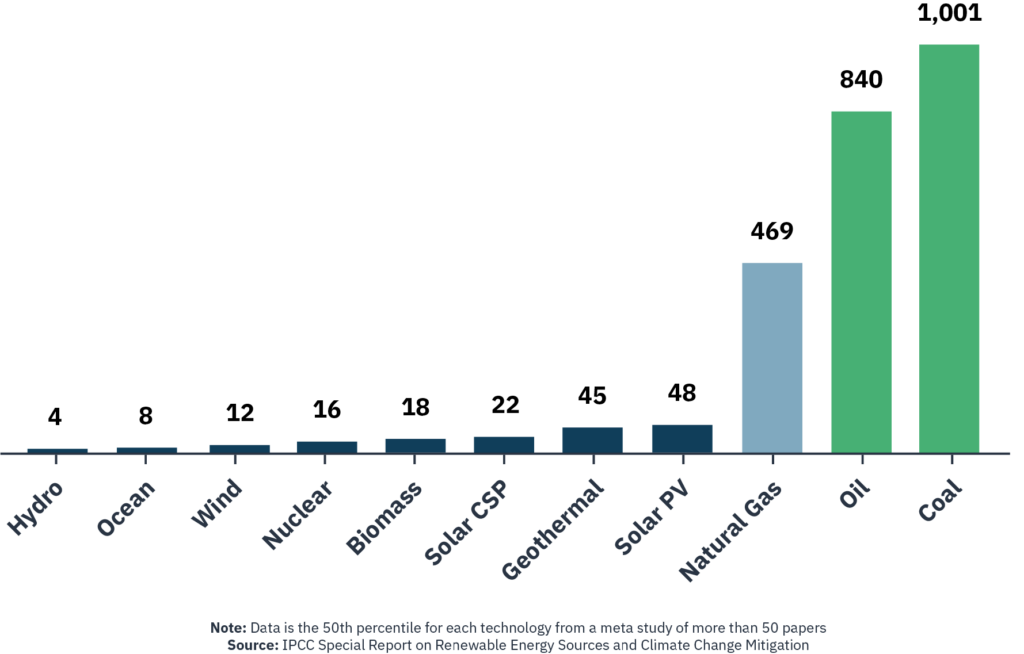

The investment opportunity to achieve transition to a Net Zero global economy is not only urgent, but also very compelling. As a fuel source, renewable energy sources release significantly less carbon than traditional, fossil fuel intensive, sources.

The Carbon Intensity of Electricity Generation

From an environmental perspective, the next 7 years are vital if we are to remain within 2 degrees Celsius warming above pre-industrial levels – the scientifically agreed limit beyond which we will experience catastrophic changes to the environment.

Whilst the Paris Agreement calls for Net Zero by 2050, in reality it is what we will have achieved by 2030 that will dictate whether we are able to gain control and manage the impact that global warming is having on our planet. However, we are seriously in danger of failing to meet the Paris Agreement’s targets and policy makers know this; creating a significant opportunity for the future for renewables.

Investment opportunities in the energy crisis

Renewables are both a compelling and an urgent investment case. They deliver energy at the lowest cost, with more supply security. This is a rapidly growing space[ix] ripe with opportunities which offers a well-distributed and diversified asset base that is not subject to the geopolitics that play a significant role in the availability, and price, of many fossil fuels[x], whilst also limiting carbon emissions that contribute to climate change.

Scale

Globally, over 390GW of new wind and 630GW of new solar PV is required per year by 2030 in order to meet mid-century Net Zero goalsxi. To achieve Net Zero by 2050, annual investment into clean energy worldwide will need to more than triple by 2030 to over £3 trillionxii. To put this in context, going forward renewables are expected to contribute to roughly two thirds of total investment in energy; the majority of this investment is expected to go into solar, wind and batteries.

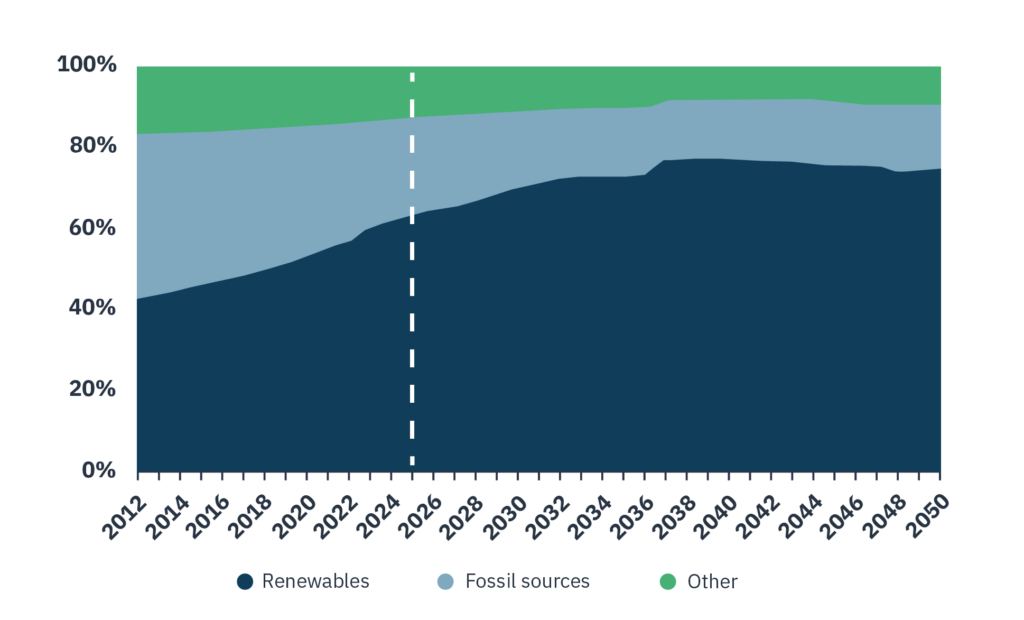

European (ex UK) energy mix (% of total generation) projections assuming EUs 2030 energy targets

Clearly the market opportunity for investing into renewables is enormous and growing – the International Energy Agency has predicted that renewables will overtake coal to become the world’s largest source off electricity generation by early 2025xiii. Private investment has the opportunity to play a critical role in facilitating technologies and innovations that will protect our planet.

It may be easy to assume that given the scale of the investment requirement laid out above, that this space would be dominated by the utilities, oil and gas majors. However, most investments into solar are typically quite small, in the tens rather than hundreds of millions. This investment space is the domain of nimble, highly specialised, investment managers. The challenge to investors is not whether there will be opportunities in this space, but in selecting the right manager.

The opportunities available can provide a range of risk-return profiles that are ultimately attractive depending on a portfolios’ needs and can vary across the investment spectrum dependent on technology, investment stage and geography.

Securing supply and government support

There has never been more support for renewables and storage. One of the reasons for this is that society and a wide spectrum of governments are becoming increasingly concerned about climate change, and with energy security if they are reliant on foreign powers to supply fuel.

With renewables providing energy security at a low cost, governments no longer have to debate with their opposition or the general public about subsidising the industry, meaning greater support from both local and European governments and populations.

Some estimates suggest that investment of over £700 billion is required into energy storage capacity, grid infrastructure for renewables and other sustainable energy innovations in Europe in order to put the available capital on par with that of the fossil fuel industry and end dependency on Russian energy importsxiv.

This means investment in renewables is on the right side of the trade and policy. Government incentives to get this right are so strong that durable, consistent support is going to be there to make investing as attractive as possible.

Risk management and diversification

Under current global decarbonization schemes half the world’s fossil fuel assets, totaling £8.1 trillion – £10.3 trillion, could become worthless by 2036xv as demand falls. The resulting excess of supply and potential stranded assets could result in long-term detrimental impacts on an investment portfolio.

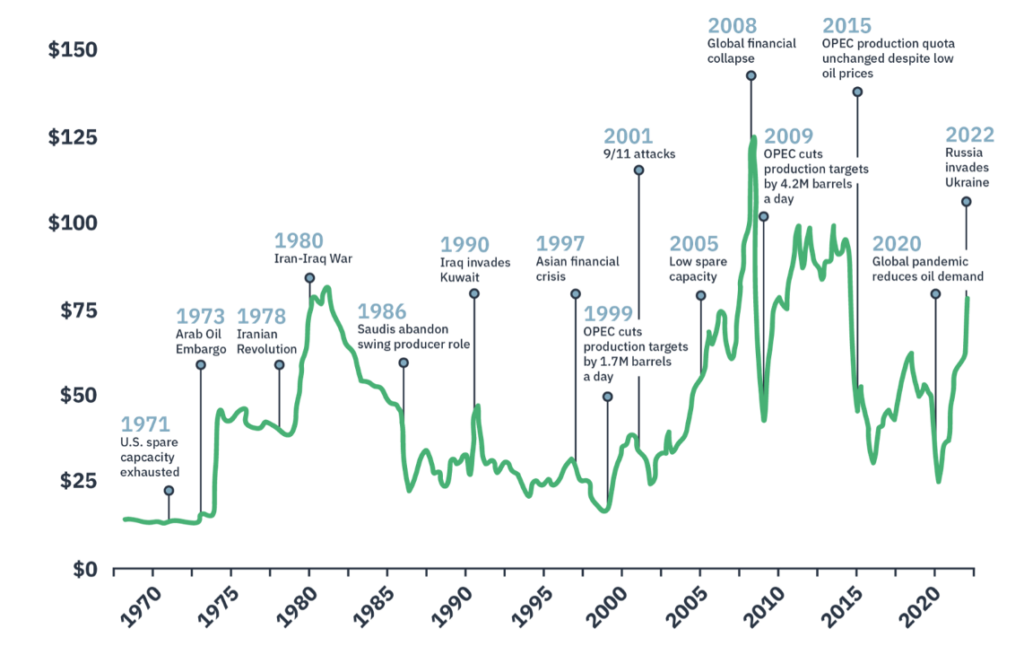

Demand and supply shocks to world oil and gas prices caused by global political and social events in recent years have illustrated the volatility of the fossil fuel market.

Geopolitical events can disrupt supply, driving prices up, while economic declines often decrease demand, causing prices to fall. This correlation to market events can result in reduced diversification benefits of incorporating energy into a wider portfolio.

Crude oil price ($/barrel) over the last 50 years

Beyond diversification, there is a broader risk management role for renewables. Without acting now to control global temperature increases, investment returns in the future will be inherently compromised without a safe and inhabitable planet.

Energy crisis or energy opportunity?

Mankind is good at making rapid changes when there is a better option in place and investors who have recognised these opportunities have reaped significant benefits – from the shift from horsepower to automobiles, to the inventions of the telephone, lightbulb or internet.

Whilst the current energy situation is one of crisis and many have witnessed tough times over the past winter, from an investment perspective this situation presents a once in a generation opportunity. The economic conditions are favourable, policy and government support are in place and the existential motivation for renewables is growing each year. Ultimately, it is up to each and every one of us to play a role in the transition to Net Zero which is essential to our planet’s survival, and private capital is critical to making this happen.

Be a part of the action. Get in touch to find out how we can support your renewable investment journey to secure attractive, diversified returns whilst creating a more sustainable and energy efficient future.

Bluefield, powering a sustainable future.

[i]UK natural Gas 2023 data via Trading Economics, 2023

[ii] Eurostat, 2022

[iii] Investment Monitor, 2022

[iv] Net Zero Climate

[v] United Nations

[vi] IRENA, 2021

[vii] BloombergNEF, 2022

[viii] Edie, 2020

[ix] https:// McKinsey, 2022

[x] Advisor Channel, 2022

[xi] IEA, 2021

[xii] IEA, 2021

[xiii] IEA, 2022

[xiv] TheMayor.eu, 2022

[xv] Nature Energy, 2021

DISCLAIMER AND IMPORTANT NOTICE

This Article is being issued by Bluefield Partners LLP (Bluefield), which is authorised and regulated in the United Kingdom by the Financial Conduct Authority, to provide certain information about Bluefield Partners and its affiliated companies (the Bluefield Group). Bluefield’s registered office address is 40 Queen Anne Street, London, W1G 9EL and its FCA Firm Reference Number is 507508.

No Offer: This Article is provided for educational and informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or financial products in any jurisdiction. This Article and the information contained therein is not intended for distribution or publication to persons outside the United Kingdom. This Article is not directed at, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or would require any registration or licensing within such jurisdiction. This Article is not a marketing communication. Recipients in jurisdictions outside the United Kingdom should inform themselves about and observe any applicable legal or regulatory requirements in relation to the distribution or possession of this Article in that jurisdiction.

Not Advice: The information contained in this Article is not intended to be, and should not be construed as, investment, financial, legal, tax or other advice, and is not a recommendation, endorsement or representation as to the suitability of any investment or financial product. You should seek independent professional advice before making any investment or financial product decision.

Past performance is not indicative of future results; no representation is being made that any investment will or is likely to achieve profits or losses similar to those achieved in the past, or that significant losses will be avoided. Any investment carries risk and the value of an investment can down as well as up. Capital at Risk.

Investments in private placements are complex, highly illiquid and speculative in nature and often involve a high degree of risk. The value of an investment may go down as well as up, and investors may not get back their money originally invested. Investors who cannot afford to lose their entire investment should not invest. Investors will typically receive illiquid interests that may be subject to holding period requirements and/or liquidity concerns. Investors who cannot hold an investment for the long term (at least 10 years) should not invest.

No Reliance: The information contained in this Article is based on publicly available information and internally developed data, but no representation or warranty, express or implied, is made as to the accuracy, completeness or reliability of such information. Any projections or other forward-looking statements contained in this Article are based on assumptions that may change and actual results may differ materially from those expressed or implied in such projections or statements. This Article and any information contained within it may be amended or withdrawn at any time without notice. Bluefield and the Bluefield Group are not responsible for any losses sustained by any party in connection with the use of this Article and the information contained therein and disclaim all liability to the extent permitted by relevant applicable law and regulation.